A new year brings a new set of tax numbers, and here are the important figures you need to know for 2022.

Don't want to read all the way through? Scroll a little further for a your quick guide.

Starting off with the hot button topic from the last 6 months…

Inflation

Did you know? Each year, most (but not all) income tax and benefit amounts are indexed to inflation. The Canada Revenue Agency announced the inflation rate used to index the 2022 tax brackets and amounts would be 2.4%.

This rate was calculated by taking the percentage change in the average monthly consumer price index data as reported by Statistics Canada for the 12-month period ended September 30, 2021, relative to the average CPI for the 12-month period ended on September 30, 2020.

Increases to the tax bracket thresholds and various amounts relating to non-refundable credits took effect on January 1, 2022.

Increases in amounts for certain benefits, such as the GST/HST credit and Canada Child Benefit, however, only take effect on July 1, 2022.

This coincides with the beginning of the program year for these benefit payments to be reported on your 2021 tax return due this spring.

Tax brackets for 2022

All five federal income tax brackets for 2022 have been indexed to inflation using the 2.4% rate (outlined above).

The 2022 federal brackets are:

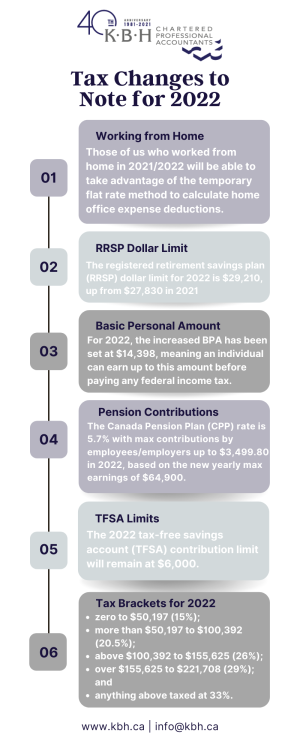

- zero to $50,197 of income (15%);

- more than $50,197 to $100,392 (20.5%);

- above $100,392 to $155,625 (26%);

- over $155,625 to $221,708 (29%); and

- anything above that is taxed at 33%.

Basic personal amount (BPA)

The BPA is the amount of income an individual can earn without paying any federal tax, and for 2022, the increased BPA has been set at $14,398, meaning an individual can earn up to this amount in 2022, before having to pay any federal income tax.

The value of this federal credit for taxpayers earning more than this amount is calculated by applying the lowest federal personal income tax rate (15%) to the BPA, making it worth $2,160. (Because the credit is “non-refundable,” it’s only worth the maximum amount if you otherwise would have paid that much tax in the year.)

Government pension contributions

The Canada Pension Plan (CPP) rate for 2022 is 5.7% with maximum contributions by employees and employers set at $3,499.80, based on the new yearly maximum pensionable earnings of $64,900 (with a $3,500 basic exemption.)

Self-employed Canadians must contribute twice the amount, so their maximum CPP contribution for 2022 will be $6,999.60, up from the 2021 amount of $6,332.90.

EI premiums

Employment insurance premiums are also rising, with a contribution rate for employees of 1.58% up to a maximum contribution of $952.74 on 2022 maximum insurable earnings of $60,300.

Tax-Free Savings Account (TFSA)

The 2022 TFSA contribution limit will remain at $6,000 for the fourth year in a row. Why? Because in 2015, the government announced that the annual TFSA limit would be fixed at $5,000, indexed to inflation for each year after 2009, but rounded to the nearest $500. In other words, once the incremental indexed annual TFSA contribution limit hits $6,250, it will jump to $6,500.

The limit is expected to increase in 2023 to $6,500, provided the 2023 indexation adjustment is at least 1.5%.

The cumulative TFSA limit is now $81,500 for someone who has never contributed to a TFSA and has been a resident of Canada and at least 18 years of age since 2009.

Registered Retirement Savings Plan (RRSP)

The RRSP dollar limit for 2022 is $29,210, up from $27,830 in 2021.

Note: The amount you can contribute to your RRSP is limited to 18% of your 2021 earned income, which includes (self)employment and rental income, less any pension adjustments, up to the current annual dollar limit.

Old Age Security

If you receive OAS, the repayment threshold is set at $81,761 for 2022, meaning your OAS will be reduced in 2022 if your taxable income is more than this amount, and is fully eliminated with taxable income over $133,141.

Working from home

To close, those who continue(d) to work from home in 2021 and 2022 will again be able to take advantage of the temporary flat rate method to calculate home office expense deductions.

Under the temporary flat rate method, employees can simply claim $2 for each day they worked from home due to the pandemic. The government in December announced in its economic statement that it was increasing the maximum claim to $500 (from $400) for the 2021 and 2022 tax years.